Ultra-high-net-worth individuals (UHNWIs) often face complex challenges when managing substantial wealth. With portfolios that typically span multiple asset classes, they require a strategic approach to high-net-worth wealth management—one that accounts for diversification, market fluctuations, and long-term planning. Managing risk while aiming for growth involves more than traditional investing; it often includes integrating estate planning, tax strategies, and liquidity considerations within a broader private investment management framework.

Asset allocation at this level usually includes a blend of equities, fixed income, real estate, and alternative investments. By distributing capital across these asset types, UHNWIs can reduce concentrated exposure and better align their portfolios with their goals. Effective wealth advisory services help ensure that asset distribution remains flexible and adaptive, supporting both near-term needs and multigenerational objectives.

Asset Allocation by Wealth Status

| Asset Allocation | Ultra High Net Worth | Pension | High Net Worth |

| Cash | 10% | 3% | 2% |

| Alternatives | 46% | 24% | 22% |

| Fixed Income | 15% | 28% | 33% |

| International Equities | 9% | 26% | 15% |

| Domestic Equities | 20% | 20% | 28% |

Table of Contents

- Diversification Tactics in the UHNW Asset Manager’s Decision-Making

- Average Asset Allocation For High Net Worth Investors

- Examples of alternative investments

- Major Asset Allocation Shock

- Returns from Traditional Portfolio Mixes

- Persist and Continue Your Investment Journey

- Is There An Innovative Real Estate Investment Strategy?

- Contentment with Alternative Investment Choices

Diversification Tactics in the UHNW Asset Manager’s Decision-Making

Varied Asset Classes

For ultra-high-net-worth (UHNW) investors, achieving meaningful portfolio diversification poses unique challenges due to the sheer size of investable assets. Allocating even a small percentage can involve committing millions of dollars, increasing the risk of portfolio concentration if not carefully managed. Working with a professional through specialized wealth advisory services can help mitigate this by spreading investments across a range of asset classes and strategies tailored to the UHNW landscape.

Non-Traditional Investments

UHNW individuals often explore alternative investments as part of a diversified strategy. These may include real estate, commodities, fine art, vintage collectibles, and cryptocurrencies. While these assets can offer long-term growth potential and serve as a hedge against market volatility, they also tend to be illiquid, carry high transaction costs, and present valuation challenges due to limited market activity.

Liquidity Reserves

To protect near-term funds from market volatility, ultra-high-net-worth (UHNW) investors typically maintain a larger portion of their portfolios in liquid assets. This helps manage exposure to fluctuating conditions while ensuring readily available capital for short-term needs.

As illustrated in the asset allocation comparison, UHNW investors often hold higher absolute liquidity, even when the percentage appears modest. For example, allocating 10% of a $30 million portfolio results in $3 million in liquid assets, compared to a 2% allocation of a $1 million portfolio, which amounts to just $20,000. While the percentage may be similar, the flexibility and strategic potential of these reserves differ significantly.

Wealth advisory services may help UHNW investors manage and optimize liquidity holdings, identifying opportunities to preserve accessibility while potentially improving returns, without increasing overall risk exposure.

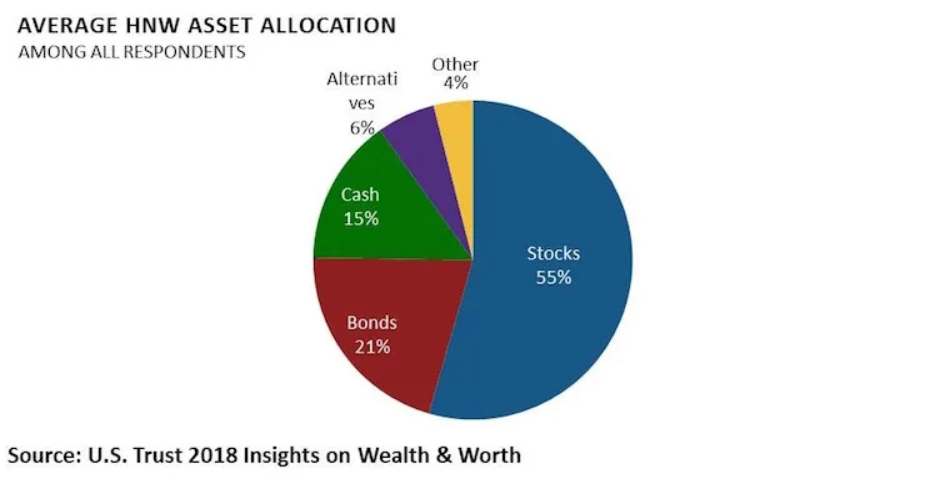

Average Asset Allocation For High Net Worth Investors

Among individuals with $3 million or more in investable assets, asset allocation trends typically favor a diversified approach. On average, portfolios are allocated as follows: 55% in equities, 21% in fixed income, 15% in cash or cash equivalents, 6% in alternative investments, and 4% in other categories.

That said, allocation strategies often vary based on risk tolerance, liquidity needs, and investment goals. For example, some high-net-worth individuals may hold a larger portion in real estate or private market alternatives to pursue long-term growth or income opportunities outside traditional asset classes.

In recent years, certain investors have shifted part of their real estate exposure into private real estate crowdfunding platforms. This approach can offer broader access to commercial or residential projects and potential passive income opportunities, though it also carries risks related to liquidity, transparency, and market volatility. As with any strategy, aligning such allocations with your broader financial objectives is essential, and this is often guided through professional wealth advisory services.

Asset Allocation Across Four Generations of Affluent Respondents

Asset allocation preferences among high-net-worth individuals often vary not only by wealth level but also by generational outlook and investment philosophy. Notably, generational differences—and even distinctions between men and women—can influence how portfolios are constructed and managed over time.

- Millennials: Ages 21–37 (Born 1981–1997)

- Generation X: Ages 38–53 (Born 1965–1980)

- Baby Boomers: Ages 54–72 (Born 1946–1964)

- Silent Generation: Ages 73+ (Born before 1946)

Each group may prioritize different goals—from long-term growth and alternative investments to income generation and capital preservation. Understanding how asset preferences shift across generations can be valuable in shaping personalized wealth advisory strategies tailored to life stage and financial objectives.

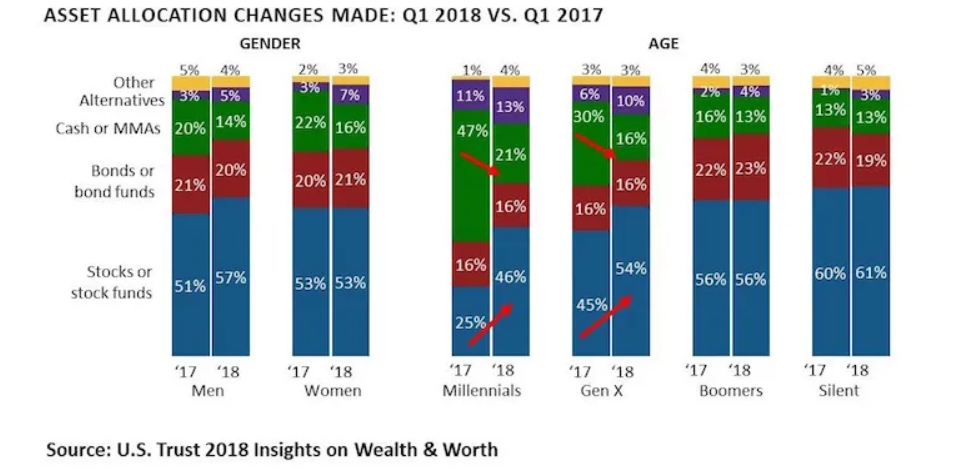

Insights from the second chart regarding how assets are distributed

- Male investors tend to allocate a slightly higher percentage of their portfolios to stocks compared to female investors, suggesting a modest difference in investment preferences.

- In 2018, every generational group—except for Baby Boomers—increased their stock holdings. This pattern may reflect a broader sense of market optimism, though some may interpret it as a potential contrarian signal.

- Millennial and Generation X investors took a more aggressive approach by increasing their stock allocations while reducing their cash positions, signaling a greater appetite for long-term growth opportunities.

- Despite this shift, millennials still maintain approximately 21% of their portfolios in cash. In a rising inflation environment and with low returns from traditional savings accounts during that period (often between 0.1% and 0.4%), this conservative stance may represent a missed opportunity for higher returns through more strategic allocation.

- Surprisingly, the Silent Generation held the highest proportion of equities in their portfolios, reflecting continued engagement with the stock market even in retirement years.

Following a strong market performance in 2017, investor sentiment across most age groups remained positive toward equities. Millennials, having largely experienced economic growth since 2010, are entering peak earning years with a long-term view, favoring stocks as a core part of their investment strategy.

Additionally, there is a growing interest among millennials in real estate, including participation in real estate syndications. This trend highlights a shift toward alternative investments as part of evolving wealth management preferences across younger generations.

Examples of alternative investments

Alternative investments provide exposure to assets beyond traditional stocks and bonds. These investments are often used within high-net-worth wealth management strategies to enhance diversification and potentially improve long-term returns. Common types include:

- Art

- Cars (collectibles)

- Coins

- Cryptocurrency

- Hedge funds

- Private credit

- Private equity

- Rare whisky

- Real estate

- Watches

While general portfolio guidelines often suggest allocating around 5% to alternative investments, this figure increases substantially for individuals with greater wealth.

According to the Chartered Alternative Investment Analyst Association, average investors may benefit from modest exposure to alternatives. However, the allocation profile changes significantly at higher wealth tiers.

A 2020 KKR survey found that individuals with at least $1 million in net worth held approximately 26% of their portfolios in alternative investments. Among the ultra-high-net-worth segment, defined as those with more than $30 million in assets, up to 50% of portfolio holdings were in alternatives.

This data highlights a key trend: as wealth increases, so does the emphasis on alternative investment strategies, often coordinated with the support of private wealth management firms.

The Performance of Luxury Goods as Alternative Investments

According to the Knight Frank Luxury Investment Index, luxury items collectively appreciated by 137% over the ten-year period ending in 2022. However, not all luxury assets performed equally. Rare whisky, for example, saw a standout increase of 373% during that period, while luxury furniture and colored diamonds experienced more modest gains of 34% and 16%, respectively.

Despite their appreciation potential, luxury goods often make up a relatively small portion of alternative investments within high-net-worth portfolios. This cautious positioning stems from several challenges. First, luxury assets tend to be illiquid and can be difficult to sell quickly, often requiring access to niche markets or specialized buyers. Second, the costs associated with acquiring, insuring, storing, and maintaining these items can be high, even when held in small quantities. Third, many luxury categories, such as fine art, are relatively unregulated and opaque, with risks that include counterfeiting and a lack of reliable historical data, making accurate valuation and due diligence more difficult. Lastly, these assets typically require a long-term holding period and are not ideal for short-term liquidity needs, which may limit their fit within certain investment strategies.

While luxury goods can offer diversification benefits, they are usually considered complementary rather than core components of a broader alternative investment strategy, particularly in the context of high-net-worth wealth management.

Exploring Digital Assets as Alternative Investment Options

Cryptocurrencies have long existed on the fringe of mainstream investing but gained notable traction beginning in 2020. Since then, digital assets have drawn both increased attention and skepticism due to significant price volatility, the collapse of several major exchanges, and regulatory uncertainties. These factors have raised questions about their long-term role within high-net-worth wealth management strategies.

Despite the challenges, interest among affluent investors remains. According to Knight Frank’s 2022 report, high-net-worth individuals allocated an average of 3% of their portfolios to cryptocurrency, less than other alternative assets such as art, cars, and wine, which held a combined average of 5%.

Digital assets are widely perceived as one of the most speculative investment categories. While 59% of high-net-worth respondents reported investing in art, only 34% viewed the NFT market as a potential area for investment, further highlighting caution around digital collectibles.

Although cryptocurrencies and NFTs may offer diversification and long-term growth potential, their inclusion in high-net-worth portfolios is generally approached with caution due to their evolving regulatory landscape and inherent volatility.

The Rising Potential of Alternative Investments for Expansion

Alternative investments continue to gain momentum as investors increasingly seek diversification beyond traditional asset classes. According to Preqin, a leading source of data and analytics in the alternative investment space, the total value of global alternative assets under management is projected to reach $23.3 trillion by 2027. This reflects a significant increase from $13.7 trillion in 2021.

Looking back further, the growth is even more pronounced. In 2010, the alternative investment market stood at approximately $4.1 trillion. A projected 470% increase over nearly two decades signals a strong shift in investor sentiment, fueled by the pursuit of long-term portfolio stability, risk management, and expanded return potential. This growth underscores a broader trend in private wealth management, where strategic diversification—including alternatives such as private equity, hedge funds, infrastructure, and real assets—is playing a larger role in wealth planning.

Rather than chasing short-term gains, the shift toward alternatives reflects a focus on building resilient portfolios that can adapt to changing economic conditions. As the financial landscape evolves, the rising role of alternatives is helping to shape how high-net-worth individuals approach long-term investment strategies.

Major Asset Allocation Shock

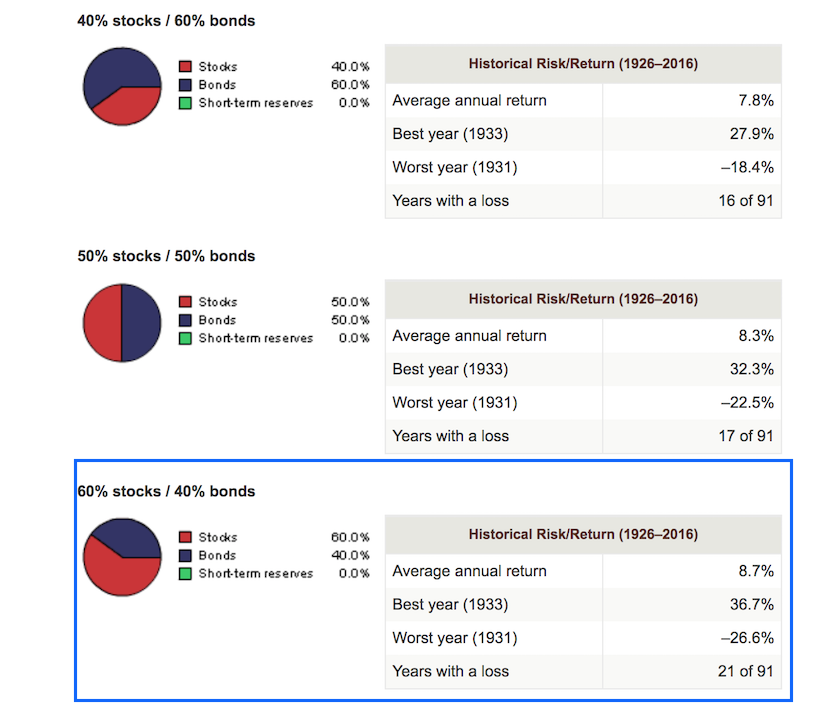

Recent data reveals that individuals aged 73 and older with high-net-worth portfolios continue to maintain a substantial allocation to equities, around 61%. This sustained exposure suggests a long-term investment mindset, even after navigating decades of market shifts and financial cycles.

Rather than representing an aggressive strategy, this allocation often reflects a balanced approach, commonly structured as a 60/40 stock-to-bond ratio. For individuals with $3 million or more in investable assets, this ratio offers both growth potential and downside protection.

Unlike younger investors who may be guided toward higher equity exposure, older high-net-worth investors often favor diversified strategies designed for income generation, capital preservation, and legacy planning. This approach has historically shown resilience through economic fluctuations and continues to serve as a core principle in private wealth management.

Returns from Traditional Portfolio Mixes

Historically, a traditional portfolio balanced between equities and fixed income has delivered an average annual return of approximately 8.7%. At that rate, an investor’s capital could theoretically double in just over eight years. However, projecting similar returns over the next decade remains uncertain due to shifting market conditions, geopolitical tensions, inflation pressures, and changing interest rates.

Reflecting on the market stagnation of the early 2000s following the dot-com collapse serves as a reminder that prolonged periods of low or negative returns are possible. More recently, in 2022, many markets experienced negative performance while interest rates rose sharply, challenging the assumptions behind bullish, long-term forecasts.

Adding venture capital into a high-net-worth portfolio introduces a new layer of complexity. These investments can offer high-growth potential by targeting emerging sectors and early-stage companies, but they also bring increased risk and volatility. For individuals pursuing alternative investments to complement traditional holdings, venture capital may serve as a source of long-term growth—but it requires careful evaluation and risk management.

Among ultra-high-net-worth individuals, particularly those with portfolios exceeding $30 million and entering their 70s or older, the need for capital preservation may outweigh aggressive growth strategies. While venture capital can still be an attractive diversification tool, many may instead focus on legacy planning, philanthropic impact, or wealth transfer strategies.

As perspectives shift later in life, financial priorities often evolve. For many investors in this stage, the role of wealth may extend beyond portfolio performance, centered more on family, values, and long-term impact. This mindset may influence how they incorporate higher-risk assets, such as venture capital, into an otherwise stable and well-diversified wealth management plan.

Persist and Continue Your Investment Journey

This analysis can serve as encouragement for those pursuing long-term investment strategies. While a heavily stock-weighted portfolio may not be necessary for every investor, maintaining a stock allocation between 51% and 100%—appropriately adjusted based on age, risk tolerance, and financial goals—remains a widely supported approach.

A balanced strategy might include a moderate stock allocation, such as 55%, complemented by a 10% allocation to alternative investments, especially during uncertain phases of the economic cycle. As portfolios grow larger, the impact of market volatility can become more pronounced, often prompting high-net-worth investors to seek more stable, lower-volatility options as part of their wealth management plans.

For those targeting annual returns in the 5% to 6% range, a blend of broad portfolio diversification, real estate syndications, and fixed-income products like Treasury bonds and certificates of deposit may support this objective. Current yields in the fixed-income space have become more appealing and may offer a reliable income stream as part of a conservative investment mix.

Real estate continues to be a cornerstone of wealth-building for many investors. For individuals with substantial portfolios, increasing real estate exposure, especially through long-term holdings or private investments, can provide diversification benefits and potential appreciation over time. Some investors have significantly increased their real estate allocation during major market events, such as the COVID-19 pandemic, aligning this shift with long-term housing or portfolio stability goals.

Ultimately, aligning investment choices with one’s risk tolerance is essential to maintaining peace of mind. The objective is to manage your assets in a way that supports your life—not dominates it—so you can remain focused on long-term goals while enjoying daily life. A consistent, well-structured approach can help build and preserve wealth across market cycles.

Is There An Innovative Real Estate Investment Strategy?

For many individuals, a primary residence represents a neutral real estate position, offering shelter rather than serving as an income-producing asset. Expanding into real estate as an investment, however, involves acquiring additional properties with the intent of generating income or long-term appreciation.

Among high-net-worth individuals, real estate remains a prominent component of diversified portfolios. Its appeal often lies in its relative stability, tangible utility, and the potential for both rental income and long-term value growth. The combination of escalating rent and appreciating property values can serve as a strong foundation for wealth preservation and expansion.

In recent years, alternative real estate strategies—such as real estate investment trusts (REITs) and real estate crowdfunding—have gained traction among those seeking exposure without direct property management. These approaches allow for broader diversification across regions and property types, providing access to income-generating real estate through a more passive and scalable model.

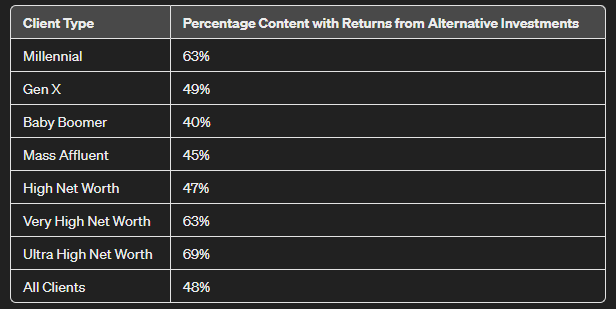

Contentment with Alternative Investment Choices

According to recent data from EY, younger and wealthier investors report higher levels of satisfaction with the performance of their alternative investments. The survey revealed that 63% of millennial respondents expressed contentment with the returns on their alternative assets, compared to just 40% of baby boomers, highlighting a notable generational divide in perception.

This disparity may reflect broader differences in investment strategies and risk tolerance. Younger investors tend to be more receptive to non-traditional asset classes and are often willing to embrace higher volatility in pursuit of growth and diversification. This openness to innovation and risk may partly explain the higher satisfaction levels among younger demographics engaging with alternative investments.

In terms of wealth segments, the survey also found a clear upward trend in satisfaction corresponding with net worth. 45% of mass affluent individuals indicated satisfaction with alternative investment outcomes, rising to 63% among very-high-net-worth individuals, and peaking at 69% for ultra-high-net-worth investors. This suggests that greater financial capacity may enhance access to a broader range of opportunities and strategies, leading to more favorable results and experiences.

Access to specialized investment vehicles, increased financial literacy, and the ability to absorb risk may all contribute to the elevated satisfaction levels reported by wealthier individuals. As portfolios grow in size and complexity, alternative assets often play a larger role, particularly among investors seeking diversification beyond traditional stocks and bonds.

Overall, EY’s findings indicate that alternative investments are becoming an increasingly important element of high-net-worth portfolios. While satisfaction varies across demographics, the data points to a growing acceptance of non-traditional investments as viable tools for long-term wealth growth and portfolio diversification.

In summary, effective asset allocation for UHNWIs involves balancing a diverse portfolio that includes equities, fixed income, real estate, and alternative investments. The key to optimizing such a portfolio lies in strategic diversification, careful risk management, and the thoughtful integration of non-traditional assets to support both growth and resilience. By adhering to these principles and adjusting to the changing investment landscape, ultra-high-net-worth individuals can work toward preserving and growing their wealth across generations.

Ultimately, the objective is to build a lasting legacy—one that demonstrates both financial discipline and a strong awareness of broader economic dynamics.